2017 China's smart driving industry development trend forecast

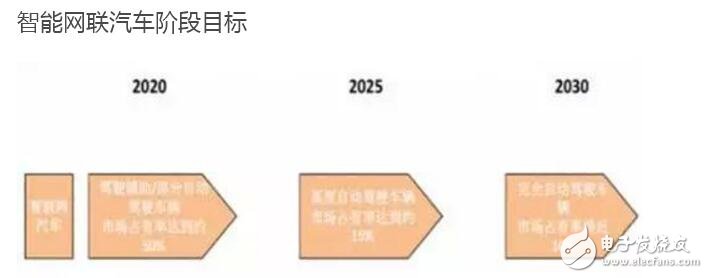

In 2030, the intelligent networked automobile industry chain and intelligent transportation system were basically built, and the rate of automatic driving and fully automatic driving of new vehicles was 80%. According to the plan of “Technology Roadmap for Energy Saving and New Energy Vehiclesâ€, in 2020, the independent innovation system of intelligent networked vehicles will be formed, and the construction of smart cities will be initiated. The market share of driver assistance/partially autonomous vehicles will reach 50%; by 2025, the market share of highly self-driving vehicles will reach about 15%; by 2030, the intelligent network of automobile industry chain and intelligent transportation system will be basically established. The rate of automatic driving and fully automatic driving is 80%, and the market share of fully self-driving vehicles is close to 10%.

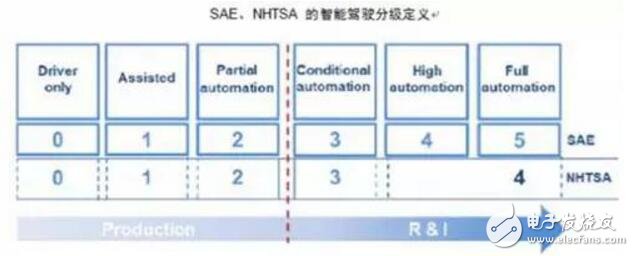

Intelligent driving can be divided into different levels according to the allocation of vehicle control rights and safety responsibility. The grading standards vary from organization to organization: the standards of the American High Speed ​​Institute (BASt), the National Highway Traffic Safety Administration (NHTSA), and the International Society of Automated Mechanical Engineers (SAE) are generally the same, with slightly different levels. Among them, the SAE classification is the most detailed, and the unmanned technology is divided into 0 to 5 levels, corresponding to full manual driving, assisted driving, partial module automation, automation under certain conditions, highly automated and fully automated driverless. NHTSA classifies highly automated and fully automated driverless as Class 4. The 0-2 level is still dominated by manual driving, requiring the driver to observe the surrounding driving environment; at level 3 and later, the intelligent driving system observes the surrounding environment.

The automotive industry is currently at level 1-2 and is expected to be fully automated in 2020-2025. At present, Level 1 and Level 2 assisted driving have matured mass production, including Level 1 warning warning function lane departure warning LDW, front collision warning FCW, blind spot detection BSD, traffic sign recognition TSR, etc., and level 2 intervention aid function adaptive cruise ACC, lane keeping assist LKA, emergency automatic brake AEB, intelligent high beam IHC, automatic parking AP, etc. The 3-level integrated function autopilot has sufficient technical reserves, such as Toyota's road autopilot assist AHAC, Tesla's autopilot Autopilot, and GM's Super Cruise, which are expected to be mass-produced between 2018 and 2020. Highly automated driving has entered the trial vehicle phase and is expected to reach mass production levels by 2020. Ultimately fully automated driving is expected to be achieved in 2025.

Intelligent driving grading

Intelligent driving will enter a period of rapid development, differentiated competition, and external technology companies enter and promote at the same time. China's smart driving development is relatively fast, mainly benefiting from 1) intensified competition in the whole vehicle, and increased intelligent configuration to achieve differentiated competition. After 2010, China's auto sales entered a period of steady growth, with a compound annual growth of 5-8%, and the competition in the vehicle industry intensified. Intelligent driving technology 360 vision, lane departure, automatic braking, adaptive cruise, embedded driving recorder, etc. can greatly enhance the driving experience and fun, and enhance the sense of automotive technology, becoming the main way for OEMs to achieve differentiated competition; 2 The external technology companies represented by Tesla are driving smart driving. By applying communication technology, electronic technology and Internet technology to the automobile industry, they have brought huge impacts and constantly refreshed consumers' expectations for automobiles. The Tesla autonomous driving version has been assembled in production cars by the end of 2015. Chinese-funded technology companies such as Weilai Automobile, Harmony Futeng and LeTV are expected to launch mass production products in 2017-2018.

Intelligent driving configuration for typical models

Outsourcing is the main way for the transformation and upgrading of component companies, especially overseas mergers and acquisitions. At present, the experience and advantages of most parts companies in China are concentrated on traditional auto parts. As a new field of rapid development in recent years, smart driving has become the main way for component companies to transform and upgrade. Especially with the original accumulation of the rapid development of China's auto market in the past fifteen years, and the support of the domestic capital market, it is expected that overseas mergers and acquisitions will continue to increase.

Mergers and acquisitions of overseas component giants in smart driving in the last two years

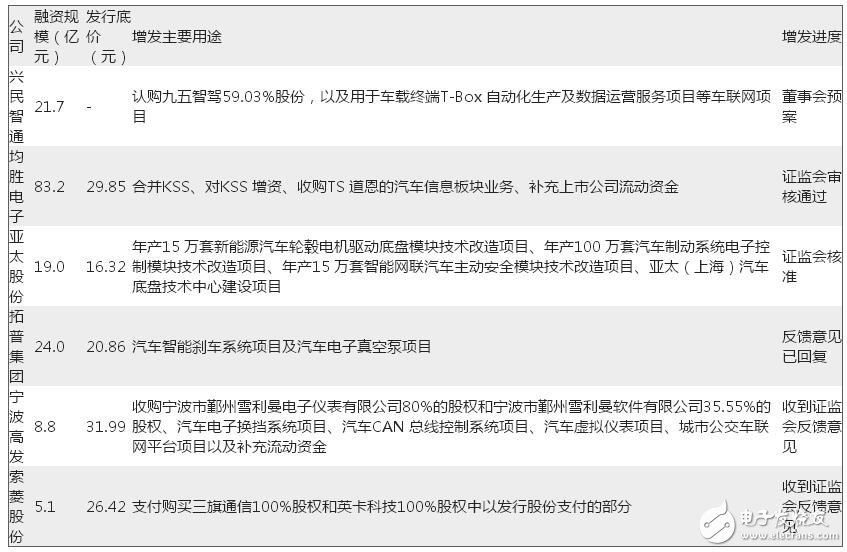

2015-2016 Parts and Components Listed Companies' Major Capital Operation Statistics

For Xiaomi Glass,Xiaomi Mi A2 Oca Glass,Touch Screen Front Glass For Xiaomi,Xiaomi 11 Front Glass

Dongguan Jili Electronic Technology Co., Ltd. , https://www.jlocaglass.com